The State of The Sustainable Aviation Fuel (SAF) Company Ecosystem

The aviation industry is facing its greatest challenge since the dawn of the commercial aircraft era in the early 1950s.

The world is turning to governments and businesses to reduce the human impact on climate change. The aviation industry, in particular, is under more pressure than ever before to slash its nearly 1 Gt in annual CO2 emissions, which amount to roughly 3% of global CO2 emissions from fossil fuel combustion. Alarmingly, this figure only represents the obvious impacts of aviation on the climate. Research suggests the climate impact of all propulsion-related emissions could be two to four times greater than those of CO2 emissions alone.

In recent years, ambitious climate objectives have been set with the intention of creating a much-needed regulatory framework for sustainable air travel, which, for example, includes:

The International Civil Aviation Organization (ICAO) agreed to cut CO2 emissions from air transport in half by 2050 (compared to the base year of 2005 when the agreement was set).

During its 77th Annual General Meeting, the International Air Transport Association (IATA) approved a resolution for the global air transport industry with the goal of achieving net-zero carbon emissions by 2050. For this to happen, a minimum of 1.8 Gt of carbon generated by a projected 10 billion passengers must be abated in 2050.

"Achieving net-zero is a colossal challenge for commercial aviation, both technologically and financially. IATA’s commitment, therefore – though some might say long overdue - is a courageous step. It is also a timely reminder that airlines can only be as sustainable as the system they operate in. Airlines don’t build planes, they don’t operate airports, manage airspace, or produce SAF, batteries or hydrogen. That is why community-building in the aviation industry and the adoption of a common agenda is more important than ever right now to deliver the energy transition that is needed. This also requires governments to step up to the plate with supportive policy measures”,

comments Sustainable Aero Lab mentor Andreas Hardeman, who has spent almost 20 years working on Environmental Policies at IATA in his career.

The big question is—how could this be made possible?

Until the 2040s at the earliest, the effective application of low carbon technologies, such as electric and hydrogen propulsion, is unlikely to be in dominant use. Should electric and hydrogen-based flying become a reality in the next 20 to 30 years, both of these technologies would only impact short-haul flights. Meanwhile, intercontinental flights would continue to demand some form of combustion-based jet fuel due to insufficient energy density levels of lithium-ion batteries. That is unless battery fundamentals are radically revolutionized, which is doubtful.

“SAF, if made from waste or synthetically, is probably the only viable solution to dramatically decrease the carbon emissions for long distance aviation. Today, SAF is only available in minuscule amounts, and often comes from sources competing with food stock. The challenges in supplying truly sustainable fuels remain gigantic with scaling production and lowering cost”,

illustrates Sustainable Aero Lab’s Co-Founder and CEO Stephan Uhrenbacher.

So, is there any realistic way forward for the aviation industry?

Sustainable Aviation Fuel (SAF) has been widely recognized as the only feasible option for the industry to achieve its sustainability targets in the coming decades. In other words, SAF is the industry’s primary means of providing a cleaner source of fuel to power the world’s aircraft fleets and enable billions of annual air travelers to lower the climate impacts of their journeys across the planet.

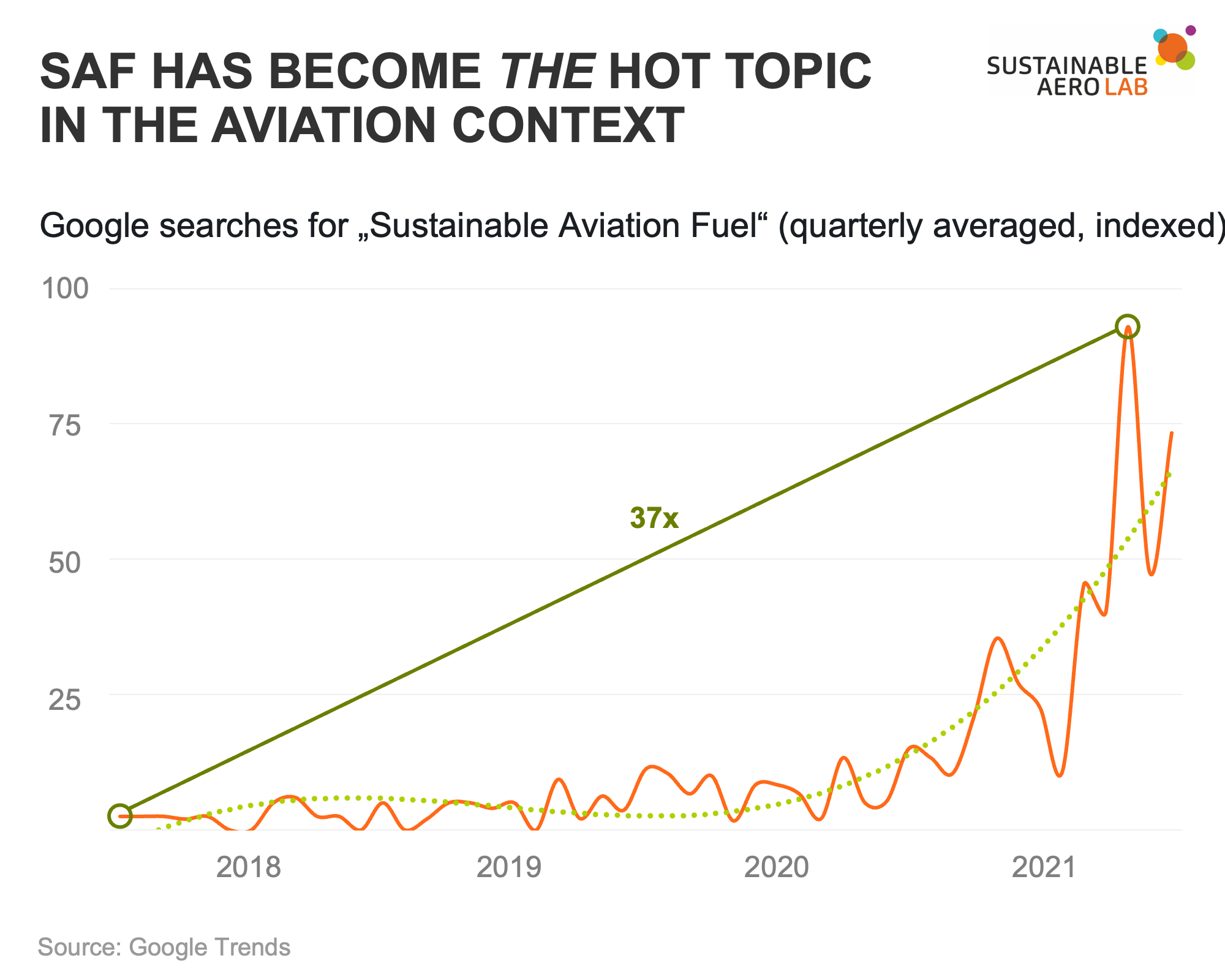

It’s no wonder SAF has become so widely discussed, making its way from internal industry talks to garner mainstream media attention. In fact, the number of Google searches for “Sustainable Aviation Fuel” skyrocketed in 2021.

When looking back over the past couple of years, it’s clear a new mindset has been ushered in. 2020 was the year that net-zero became the strategic aim for sustainable aviation and 2021 was the tipping point for SAF to be recognized as the most logical way to achieve it.

The “SAF-path” into a more sustainable aviation future also becomes evident when looking at how airlines have thus far addressed the pressure to reduce carbon emissions.

Every major carrier in the world has recently launched SAF initiatives. These include partially SAF-powered demonstration flights, SAF purchasing agreements with energy and fuel providers, SAF-based compensation programs for customers (e.g. Compensaid by Lufthansa), alongside other partnerships dedicated to enabling SAF use. These new measures, adopted to address concerns about the ongoing climate impacts of the aviation industry, have been heavily marketed to the public.

Here are a few recent SAF airline announcements, which were shared in just the last few months:

On Nov. 10, 2021, the first British Airways flight to the United States after 18 months of travel restrictions was powered by a 35% blend of sustainable aviation fuel—the first commercial transatlantic flight to be operated with such a high SAF contribution, according to British Airways.

On Dec. 1, 2021, United Airlines flew a plane full of passengers from Chicago to Washington, D.C. with one engine 100% powered by SAF made from corn sugar. This was a historic first, according to the airline.

On Dec. 15, 2021, Qantas announced, it began using blended SAF on its flagship London flights, in turn reducing carbon emissions on flights departing from London by 10%.

On Dec. 17, 2021, Malaysia Airlines operated its inaugural SAF flight, which departed Amsterdam Airport Schiphol to Kuala Lumpur using a blended mixture of approximately 40% SAF made from used cooking oil.

On Jan. 20, 2022, Oneworld alliance members announced they would purchase more than 350 million gallonsof blended sustainable aviation fuel over a seven-year period beginning in 2024 for operations at San Francisco International Airport.

At present, airlines are only allowed to use a maximum of 50% SAF on board flights. However, this could change soon. Promising results were yielded from the initial findings of a 2021 study conducted by Airbus, Rolls-Royce, Neste, and the German research center DLR, which evaluated the impacts of 100% SAF on both engines of a commercial jet. Therefore, experts anticipate future aircraft and engine generations will be capable of handling 100% SAF.

This would be an important milestone and one that could further incentivize governments and regulators to launch compulsory SAF fuel contributions. For example, in Europe, a compulsory SAF proportion of 2% by 2025 has been proposed for all flights departing within and from the continent. While it may not sound like much, that 2% undoubtedly is, especially when you consider that nearly all commercial flights today contain no SAF whatsoever.

So, why are airlines not legally obligated to use more SAF?

In the grand scheme of things, stronger SAF contribution requirements won’t necessarily lead to a more sustainable SAF future. The industry-wide introduction of a mandatory SAF contribution for all flights operating today is simply not feasible, largely due to supply constraints. At present, global SAF volume remains extremely low with SAF accounting for less than 0.1% of the aviation fuel market, according to the IATA (more on that below).

Fortunately, in recent years, a vibrant ecosystem of SAF companies has formed, which could shift the aviation paradigm and take SAF capacity, distribution, and marketing to a whole new level. Using the first-ever comprehensive SAF company mapping, we will introduce you to the most relevant SAF stakeholders. Before that, let’s take a look at the basic facts surrounding SAF.

Sustainable Aviation Fuel 101

-

What is SAF?

Sustainable aviation fuel, often called “renewable jet fuel” or “alternative jet fuel,” is made from renewable sources, including used cooking oil, municipal waste, and woody biomass alongside electric energy (in the case of synthetic SAF). In addition to these sources, SAF can be derived from energy crops, such as fast-growing plants and algae. SAF is very similar in composition to traditional fossil jet fuel.

SAF is considered a safe, reliable fuel, which has the potential to reduce lifecycle emissions by up to 80% in comparison to conventional aviation fuel. This largely depends on the sustainable feedstock used, production method, and the supply chain to the airport. Interestingly, SAF is a “drop-in fuel,” which means it can be blended with fossil jet fuel. In turn, the blended fuel requires neither special infrastructure nor equipment changes. Given this, SAF can be shipped in the same pipelines as conventional jet fuel and adopted with minimal retrofit costs.

SAF, as it is currently known, was first used by the aviation industry in 2008. According to the IATA, since 2016, more than 370,000 flights have taken off using a SAF contribution.

The concept of SAF is similar to ethanol and not a new idea in and of itself, as Forbes rightfully concludes. Biomass fuel development goes back all the way to the 1850s. In fact, much of the global gasoline supply contains ethanol, which is often made from corn and sugarcane. But there’s a critical difference between ethanol and SAF when it comes to air travel. Jet fuel packs a lot of energy for its weight and it’s exactly this energy density that has allowed for commercial flight application, as BP puts it.

What exactly makes SAF sustainable?

SAF does not reduce “tailpipe” emissions from burning fuel in-flight. The calculated reductions in greenhouse gas emissions come from the life cycle of jet fuel.

The consumption of conventional jet fuel releases fossil CO2, which pulls it from the ground and adds it to the total carbon in the biosphere. Meanwhile, burning SAF returns carbon to the atmosphere that had previously been absorbed by plants or that would have been released as industrial waste gasses or household garbage.

The result is a net “well-to-wake” reduction in life-cycle CO2 emissions. This can be as high as 80% for the SAF produced from biomass (e.g. cooking oil). As a result, commercial flights powered by SAF are coined “net-zero,” as opposed to “zero emissions”. The latter would only be possible through zero emissions at the tailpipe as in the (projected) case of a hydrogen-powered aircraft.

However, synthetic fuels produced from captured CO2 and renewable electricity can reach well-to-wake reductions of 100% relative to fossil jet fuel. Some feedstocks even promise to be carbon negative. Researchers at the US National Renewable Energy Laboratory report that SAF made from food waste has the potential to reduce net carbon emissions by upwards of 165%. This reduction claim is based on preventing food waste rotting in landfills from releasing methane, a greenhouse gas 20 times more potent than CO2.

Why SAF cannot be the only solution

While SAF has clear advantages in comparison to conventional jet fuel, it has its own shortcomings. As previously discussed, SAF does not provide a zero-emission future for aviation. Therefore, innovation cannot be focused on SAF alone. As some critics have pointed out, the sector's embrace of SAF distracts from the need to invest in more radical, truly zero-emission technologies, such as electric and hydrogen.

On top of this, skeptics tend to question just how effective the scale of emissions savings will be. Especially so, given not all types of SAF input factors produce the same life-cycle CO2 reductions. As well, these cynics warn that as feedstocks are limited, SAF investment will not fully displace the sector's reliance on fossil fuels.

Such input factor critiques must be taken seriously. Some early efforts to produce renewable fuels using sources like palm oil caused more harm than good. This example drove changes in land use and diverted resources from producing food.

These drawbacks tend to pile up when choosing so-called 1-G feedstocks given the majority of these food crops not only have high water and nutrient demands but compete for land with food producers. To circumvent the scarcity of land resources, expansion into forestland has been the most convenient option at the expense of deforestation and biodiversity loss.

Non-edible 2-G biomass resources can evade the food vs. fuel dilemma of 1-G feedstocks. Generally speaking, waste biomass utilization offers far greater benefits, such as the true realization of circular economies and environmental protection. With this in mind, it is clear that the aviation industry favors a shift towards waste streams that do not compete with food production. New sources are becoming available such as municipal solid waste, which would otherwise go to landfills or be incinerated, waste gasses from industrial processes, and finally, residues from agriculture and forestry.

However, all these feedstocks likely won’t be enough to sustain the amount of SAF needed by the aviation industry to meet its sustainability goals while simultaneously following sustainable practices. To reconcile this, the industry is researching further opportunities to develop SAF long-term.

Electricity generated by wind turbines or other renewable sources, for example, can be converted into liquid fuel, a process known as Power-to-Liquid (PtL). This enables the production of SAF without using feedstock. This would be crucial because as Shell reports, it is unlikely there will be enough biomass feedstock and bio SAF production capacity to meet more than 20% to 30% of the aviation industry’s SAF requirements by 2050. As a result, synthetic SAF must be developed quickly, so it can reach a commercially relevant scale as soon as possible.

Jan Toschka, President of Shell Aviation and who has guest-mentored at Sustainable Aero Lab in the first cohort:

“Shell Aviation intends to work together with all players in the aviation ecosystem to help accelerate the sector’s pathway to net zero. We believe it is critical to scale both production and the use of SAF. When it comes to production, Shell has a clear ambition to produce 2 million tonnes of SAF a year by 2025 and is taking steps to achieve that. And when it comes to helping increase the use of SAF, Shell is taking a forward-thinking approach to ensure the right supply infrastructure and capabilities are in place to get SAF molecules to where its customers are flying from.”

Why the aviation industry needs SAF

The biggest advantage of SAF is that it can be used as a drop-in replacement for current fossil fuels. Therefore, existing combustion engines don’t require modification. In fact, choosing SAF as the primary decarbonization method has the advantage of avoiding aircraft and airport infrastructure redesign altogether. There is simply no better long-hanging alternative to SAF.

Envisioning SAF as an immediate, viable solution to the sustainability challenge becomes easier when you consider the aviation industry’s concrete roadmap on how to become net-zero by 2050.

According to IATA industry experts and energy providers like Shell, SAF has to account for upwards of 65% of the reductions in aviation emissions by 2050. This needs to happen if the aviation industry wants to fully realize its net-zero target. With such high expectations, it’s important to consider the challenges SAF currently faces.

The SAF challenges for aviation

Production (Supply)

Right now, SAF is barely in use, which is troubling, to say the least.

According to our research, sustainable aviation fuel is still a fledgling industry with roughly only 20 million gallons (~75 million liters) produced and consumed globally in 2020, which accounts for less than 0.05% of the world’s aviation fuel use (and, in fact, significantly lower than the 0.1% reported by IATA).

Energy companies, biotech players, and startups are all part of a growing ecosystem aiming to kickstart SAF production (find out more below). However, things won’t change much in the years to come. Shell, for example, has announced its ambition to produce approximately 2 million tonnes of SAF annually by 2025. Shell even wants to have at least 10% of its global aviation fuel sales come from SAF by 2030. But this is still a drop in the ocean when considering exactly how much fuel is needed by the global aviation sector. The sheer scale of the aviation industry coupled with the volume of fuel required to make a dent in its emissions footprint is daunting.

This is a supply and capital investment problem more than it is a technology problem, though the technology needs to mature in order to run on less constrained feedstocks. According to McKinsey, a full transition to SAF is in theoretical reach. From a feedstock perspective and with the inclusion of synthetic SAF, enough raw material could be available to fuel the global aviation industry by 2030.

As Senior Vice President of Sasol’s new SAF branch, ecoFT, Dr. Helge Sachs gives an outlook on which direction he thinks the production will take:

“We believe sustainable aviation fuels produced via the Power-to-Liquid (PtL) route will be the likely choice in the long run, because CO2 is an abundant feedstock compared to other natural resources. Blue hydrogen will be an enabler in the mid-term, until enough green volumes are available. All participants along the value chain will need to be active supporters of this transition and leverage Fischer-Tropsch technologies. Sasol has responded to this development by recently creating an entirely new business unit, Sasol ecoFT”

Dr. Ulf Neuling from the Hamburg University of Technology (TUHH) and lab scientist at the Sustainable Aero Lab adds:

“The various biogenic and non-biogenic SAF options all have their individual pros and cons in the context of large-scale SAF utilization. In the long-term perspective, synthetic or Power-to-Liquid (PtL) options show a large potential in terms of greenhouse gas reduction and therefore climate impact mitigation for aviation. However, to eventually make use of this potential, the main feedstock required, namely hydrogen and carbon dioxide, have to be supplied in a sustainable manner, e.g. by using renewable electricity and direct air capture (DAC) technology. Yet the sufficient commercialization and large-scale roll-out of PtL technologies still seem unrealistic within the 2020s. Bio-based SAF could play an important role in the meantime, especially when produced from agricultural or forestry residues.”

Costs

The second major hurdle for SAF is the cost of production. Historically, airlines have suffered from low margins. Given this, carriers simply can’t afford the price of implementing widespread SAF usage at its current price level. As of today, SAF is, on average, between two and four times the cost of conventional fuel. In some cases, this figure jumps to upwards of 8 times more, depending on the SAF type and supply location. Until the industry matures and production costs drop, one form of government support or another will be required.

On the bright side, costs are anticipated to decline with further innovation and greater production. Despite this, the impact on the bottom lines of airlines will continue to be significant as illustrated on the left.

The major challenge moving forward is mobilizing investments to develop multiple new large-scale facilities to kickstart production and to lower production costs.

A growing SAF ecosystem will prove pivotal

Overview

To address the full range of challenges faced by SAF, it is critical for stakeholders from the energy and chemical industries, the investment community, technology startups, and regulatory bodies to come together and shape a viable business environment. In doing so, these stakeholders can move the needle when it comes to production scale and capital allocation. Without such major steps forward, precious time is lost.

Fortunately, in recent years, the SAF ecosystem has experienced rapid expansion with countless cross-collaborations among stakeholders, especially since 2019, when the sustainable aviation narrative gained full traction, becoming a mainstream phenomenon.

Since then, scientists, technology startups, fossil fuel, and chemical giants alike have been battling to become lead advocates and suppliers of SAF.

"It's a bit of the Wild West. You've got companies trying to get going, you've got companies maturing technologies, you've got technologies trying to make the leap to commercial before they're quite ready," concludes University of Alberta professor David Bressler, whose own advanced-stage research into the production of jet fuel from waste fats and oils was awarded a nearly $3-million federal grant in 2021, as reported by CBC News.

To better understand this “Wild West”, we, the Sustainable Aero Lab, researched and identified leading stakeholders and companies across six major categories in the increasingly heterogeneous SAF ecosystem, visualizing them in the following comprehensive overview.

The leading SAF producers

When analyzing this growing stakeholder map, it became apparent that traditional energy and chemical companies, including Neste and Shell, with their extensive fuel processing and production capacities, are the ones building the foundation for the full-scale production of SAF.

For example, at present, Neste has an annual production capacity of 100,000 tonnes of SAF, making the firm the global leader in SAF production. With Neste’s Singapore refinery expansion underway and additional investment having been made into the Rotterdam refinery, the company appears on its way to having the capacity to produce 1.5 million tonnes of SAF annually by the end of 2023.

On top of this, Neste recently acquired Mahoney Environmental, a global leader in used cooking oil recycling. The acquisition will help Neste gain access to a substantial volume of used cooking oil, alongside a platform to grow its raw material supply chain in North America.

While Royal Dutch Shell currently supplies SAF to airlines made by other companies, including Neste, the energy giant aims to produce roughly 2 million tonnes of own SAF annually by 2025, which is the largest and most aggressive target among major oil companies to date. In fact, this goal even surpasses Neste’s capacity plans.

In January 2022, ExxonMobil accelerated its role in SAF by acquiring a 49.9% stake in Biojet AS to ramp up its access to biofuels and biofuel components. These can also be applied to the aviation context in the form of SAF. Biojet plans to develop upwards of five new facilities to produce biofuels with commercial production set to begin in 2025 at a manufacturing plant to be built in Follum, Norway.

Despite these moves, energy giants face significant competition from a growing breed of post-dotcom energy startups who have transformed into established biotechnology companies over the past 15 years.

A prime example of this is the publicly traded Velocys, a biotechnology company considered one of the first startups to push forward sustainable fuels for aviation and other transport sectors. Founded in 2001, the company is now a major supplier of SAF to many of the largest carriers in the world. In November 2021, Velocys signed a 15-year offtake agreement with Southwest Airlines, guaranteeing 575 million blended gallons of net-zero SAF for the U.S. carrier.

Chemicals specialist Aemetis is another quintessential example from the growing biotech space. Founded in 2006, Aemetis recently announced plans to greatly expand its SAF production capacity, signing an agreement to purchase a 125-acre former U.S. army facility to produce SAF and renewable diesel. In October 2021, the company secured a $1 billion offtake agreement with Delta Air Lines for 250 million gallons of blended fuel containing SAF to be delivered over a 10-year period.

In addition to these growing biotech companies, the latest wave of innovative startups in the SAF space is also very promising. In the last five years alone, the sector has boomed with the founding of several new companies making headlines.

"Startups play a critical role in driving technology and innovation, often through more disruptive means than classic industry incumbents. We see this playing out through unconventional approaches to SAF production and distribution by speeding up the process of prototype testing, bringing together brilliant minds with the aligned incentives, as well as driving innovation along the entire value chain of the industry. It’s an exciting time to be a part of this industry”,

says Sustainable Aero Lab mentor Sara Jones, Senior Vice President at New Vista Acquisition Company (co-founded by former Boeing CEO Dennis Muilenberg).

It’s no wonder startups are testing and refining alternative SAF options. Meanwhile, major energy companies mostly stick to fuels produced from used cooking oil and other lipids.

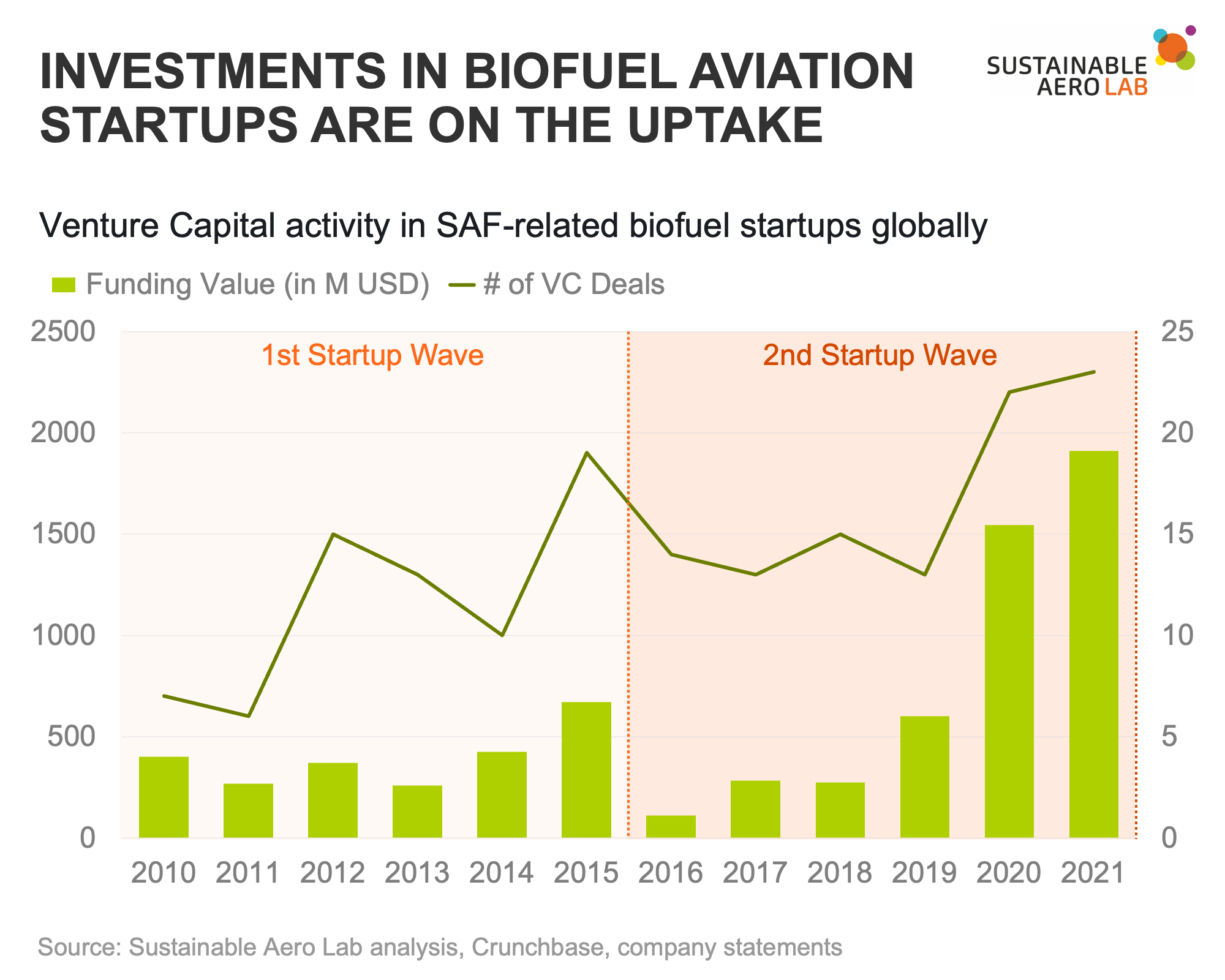

Over the past ten years, the biofuel and SAF startup ecosystem has grown in two separate waves, which can be observed by taking a closer look at venture capital investment trends.

The first SAF startup wave

The first SAF startup wave began in 2010. Five years later, $700 million U.S dollars had been invested into respective biofuel startups. This era has been dubbed the “Great Algae Biofuel Bubble,” a time during which dozens of companies managed to extract hundreds of millions in cash from venture capitalists in the hopes of extracting fuel oil from algae. Sustainable aviation fuel was one of the potential end products. However, things didn’t go according to plan. In fact, nothing close to the billions of gallons forecasted by industry experts was produced nor was there competitive pricing at all. Dozens of startups went under. Those that did survive were forced to adopt new business plans and pursue other forms of biomass with a group of companies (see many of the Late-Stage Startups in our SAF Ecosystem Overview above).

Sky NRG

One of the aforementioned surviving startups is Sky NRG, a company founded in 2010 as a joint venture between Spring Associates, EME, and KLM Royal Dutch. For 10 years, Sky NRG experimented and developed proprietary technology, for instance, by taking municipal solid waste in landfills and capturing the emitted methane to create SAF. In doing so, the company supplied dozens of aviation companies, including Alaska Airlines and Boeing, however, only with small quantities of SAF. But in 2020, Sky NRG made headlines when the firm raised anundisclosed amount of venture fundingfrom Noordelijke Ontwikkelings Maatschappij, which will allow Sky NRG to hyper-scale its production output. The

SG Preston

Founded in 2012, Philadelphia-headquartered SG Preston is another startup that persisted despite the odds. In September 2021, the company signed a commercial agreement with JetBlue to speed up its transition to SAF with plans for the largest-ever supply of SAF in New York airport history for a commercial airline. Under this agreement, SG Preston will deliver a minimum of 670 million gallons of blended SAF to JetBlue to fuel its flight operations at JFK, LGA, and EWR, helping the airline avoid approximately 1.5 million metric tonnes of CO2 emissions. JetBlue expects to invest more than $1 billion into the purchase of SAF over the term of this agreement at a price competitive to traditional Jet-A. This marks the airline’s largest single jet fuel contract.

CleanJoule

CleanJoule, based in Salt Lake City, is another company that lived to see another day. This enduring startup, founded in 2009, recently received financial backing to accelerate the commercialization of its technology and advance meaningful efforts to slow climate change caused by the aviation industry. In a November 2021 deal with Cleanhill Partners, CleanJoule raised an undisclosed amount of development capital. This major win for the company came after it was awarded a contract in 2020 with the U.S. Air Force to showcase advanced SAF for hypersonic applications and signed a partnership with Gulfstream to demonstrate petroleum-free SAF in experimental flights, according to the firm’s own press release.

The second SAF startup wave

The second SAF startup wave began in 2016 (see Early-Stage Startups in our SAF Ecosystem Overview above) with more than $4 billion U.S. dollars having been raised in venture capital investments over the last 3 years alone. While this number may seem formidable, in the grand scheme it is petty change when compared to the $100+ billion U.S. dollars that have been invested in zero-emissions tech startups over the past decade (see our previous research study) or the $60 billion U.S. dollars of venture capital that were poured into climate technology globally in the first half of 2021.

Over the past few years, funding activity has been promising nonetheless. A handful of companies have played a critical role in raising SAF capacity levels.

Here are a few highlights showcasing major funding events among early-stage startups in 2021:

LanzaJet

Chicago-based start-up LanzaJet produces SAF as an alternative to petroleum-based conventional jet fuel. Founded in 2020, the company raised an undisclosed investment sum from energy giant Shell in April 2021, which joined Japanese trading house Mitsui, Canadian oil and gas firm Suncor Energy and U.K. airline British Airways as an early-stage backer in the U.S. startup.

In early 2022, Microsoft also joined LanzaJet’s cap table by investing an additional $50 million into a LanzaJet facility in Georgia that will produce jet fuel from ethanol, launching the company into startup stardom and turning it into one of the most hyped enterprises in the aviation industry addressing carbon emissions. According to Lanzajet’s own statements, the firm is about to complete on-site engineering at its Freedom Pines Biorefinery with plans to start producing 10 million gallons of SAF and renewable diesel annually from sustainable ethanol, including from waste-based feedstocks, in 2023.

Alder Fuels

Alder Fuels is another example of a startup that catapulted itself to the SAF infamy in just a few months. The company was founded in 2021 as a clean-tech development and production company spearheaded by CEO Bryan Sherbacow who previously co-founded AltAir Fuels—the company responsible for the world’s first refinery designed to produce SAF back in 2009 that was later acquired by World Energy. A few months ago and not long after being founded, Alder Fuels entered a commercial partnership with United Airlines and Honeywell. As part of the arrangement, United Airlines has purchased 1.5 billion gallons of SAF from Alder Fuels, the largest publicly announced SAF agreement in aviation history.

Wasteful

Wasteful is a next-generation waste-to-fuel business that converts municipal waste into SAF. In February 2021, the startup received financial backing from private-aviation company Netjets, which committed to the purchase of 100 million gallons of WasteFuel’s SAF over the next 10 years.

More SAF startups to watch

The SAF startup ecosystem continues to dazzle with technology and innovation. Here are a few more companies to watch that are transcending traditional approaches to sourcing and producing SAF:

Dutch startup Zenid, founded in 2021, aims to build the world’s first industrial demonstration plant for sustainable aviation fuels made from air. Located right in the heart of Europe’s largest kerosene trading area, Rotterdam, Zenid is exploring technology development with companies such as SkyNRG, alongside the Rotterdam The Hague Airport.

Other startups are focused on “synthetic fuels,” which are not always fully in line with the standard definition of SAF but still showcase the level of innovation present in the alternative fuels marketplace. For example, Germany’s Caphenia has registered more than 150 patents across the globe for a Power-and-Biogas-to-Liquid (PBtL) process to convert CO2 and biogas into renewable synthetic fuels.

Final thoughts

There is no single solution when it comes to increasing the supply and usage of SAF. Rather, there needs to be a robust combination of capital investments, massive production buildup, efficiency gains across the supply chain to drive down costs as well as policy incentives. On top of this, the SAF ecosystem needs time to develop so it can yield effective, comprehensive outcomes for the aviation industry.

Without a doubt, the SAF company ecosystem is a fascinating and exciting space. Especially so, during these unprecedented times. As we look towards the future, let’s hope SAF can be produced on a far greater scale, propelling the aviation industry towards sustainable solutions to climate impacts. Aviation is often perceived as an industry that will decarbonize later than others. However, with these insights in mind, there’s plenty of room for players to step up to the plate and score those much-needed home runs.

A transition to carbon-neutral flying is undoubtedly possible and SAF continues to be the most promising decarbonization way forward over the next two decades.

If you are a startup founder or investor in the SAF arena, don’t hesitate to reach out.

About the Sustainable Aero Lab

The vision of the Sustainable Aero Lab is to make climate-neutral aviation a reality.

We globally identify and help startups and projects that can prove their tangible impact on the reduction of the climate footprint of aviation.

We do this by bringing together startups with experienced mentors and investors for one-to-one coaching, opening doors and finding customers, new projects and partners. Participation in the Lab is free to all startups and admissions are rolling, without deadlines.

In addition, Sustainable Aero Lab serves as a platform to publicly discuss and promote zero-emission technologies in aviation, including fields such as SAF and hydrogen.